A year ago, we launched PropTech1 Ventures to establish the first independent venture capital fund in German-speaking Europe that focuses on the digitalization potential of the real estate industry, investing in the most promising PropTech startups in Europe.

One year, five investments, and more than 200 analyzed startups later, we have created a data set that allowed us to make some statistical statements about the European PropTech ecosystem at our second Family Day on 21 March 2019 in Berlin-Kreuzberg on the occasion of our first anniversary.

We do not claim this to be a representative study, but a sample of a good 200 companies does seem to represent a certain critical mass, especially since there are currently comparatively few reliable surveys with substantially larger samples. Here are our findings.

Size of the investment universe

When PropTech1 was still in its inception phase in 2017, and we wondered whether a fund specializing solely in PropTech startups would be a good idea at all, our biggest concern was that such a sharp focus would simply not offer enough investment opportunities, i.e. the investment universe for a highly selective venture capital fund would simply (still) be too small.

About a year and a half later, we can report that this concern was unfounded because even after we analyzed 200 PropTechs from our deal flow, we have by no means the impression that we will no longer see any new companies. According to market estimates, there are currently around 1,500 PropTechs in Europe, a figure that is well in line with our impression even though we can also observe quantitative and qualitative growth in the investment universe from year to year.

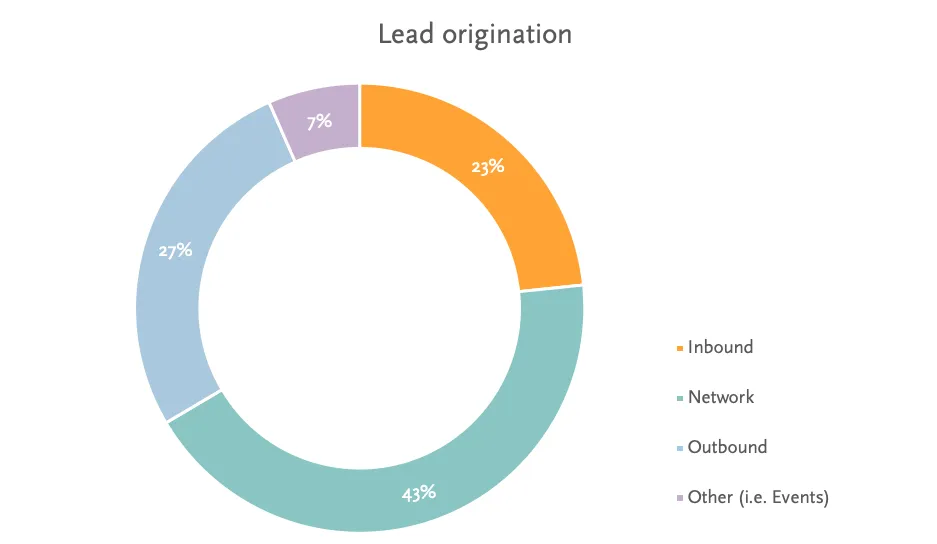

Composition of the PropTech1 deal flow

About half of our deal flow originates from our own “network”, i.e. in particular our investment and management team, our six venture partners, and more than 20 shareholders from the real estate industry and serial entrepreneur scene as well as co-investors, who specifically approach us for investment opportunities.

Experience has shown that this “original deal flow” also represents the most promising source of deals. Correspondingly, we generated four of our five investments in this way in the first year. A good quarter of the leads were generated by active enquiries from our investment team (“outbound”), which deemed the respective PropTechs relevant by researching individual market sectors and peer groups and subsequently contacted them. One of five of our 2018 investments came about in this way. The last quarter of the leads are the so-called cold requests (“inbound”) — startups contacting us directly without a recommendation from the network.

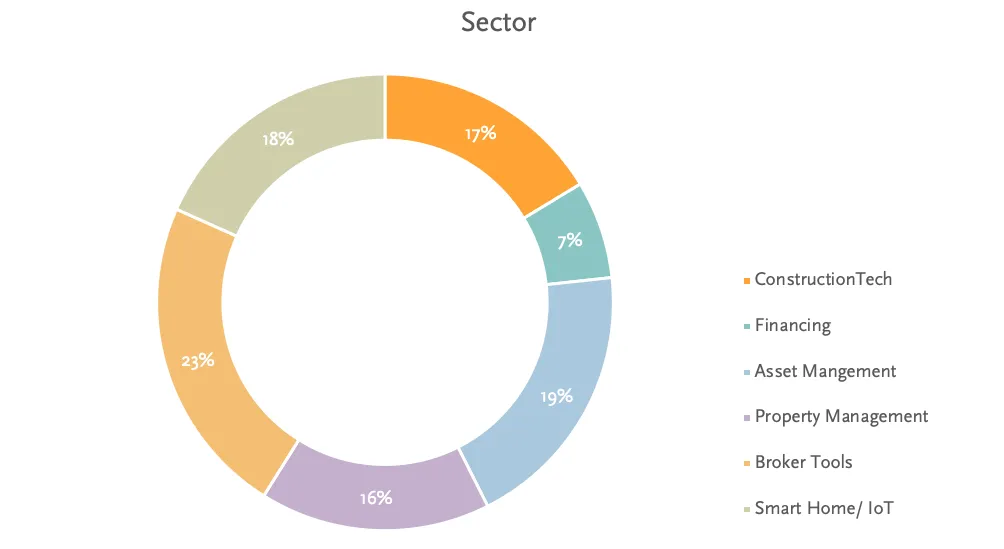

We have divided the thematic universe of the various PropTech sub-segments into the sectors ConstructionTech, financing, asset management, property management, broker tools and smart home / IoT. The largely even distribution between the individual sectors shows that founders see digitalization potential in all segments of the real estate value chain.

On the basis of the data set described above, we can derive the following five theses:

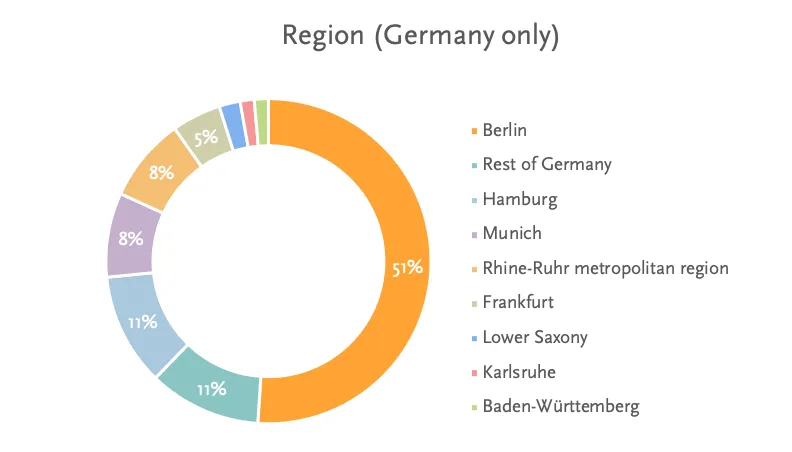

1. Berlin is the PropTech capital of Germany

Even though our sample may be “biased” primarily by our own presence in Berlin, the German capital and startup hot spot also seems to be at the forefront of the PropTech ecosystem. More than half of the companies we have looked at are based in Berlin. Hamburg, the Rhine-Ruhr metropolitan region, and Munich also stand out with approx. 10% each. Apart from Frankfurt with a 5% share, we do not see any other PropTech centers in Germany.

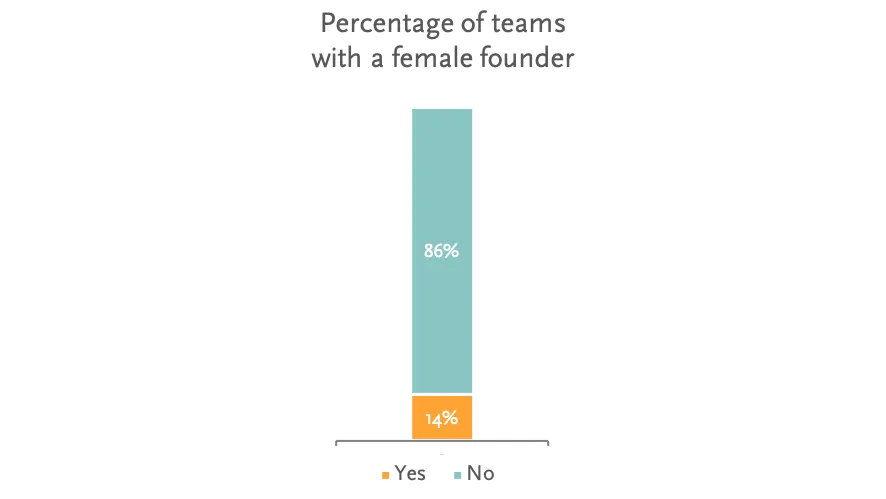

2. Women are severely underrepresented in the PropTech sector

Unfortunately, only 14% of all the PropTechs we have examined have a female founder on board. As unsatisfactory as this figure is, it comes as little surprise, as it is consistent with the results of the German Startup Monitor, which shows similarly low figures for the entire German startup ecosystem year after year (2018: 15%).

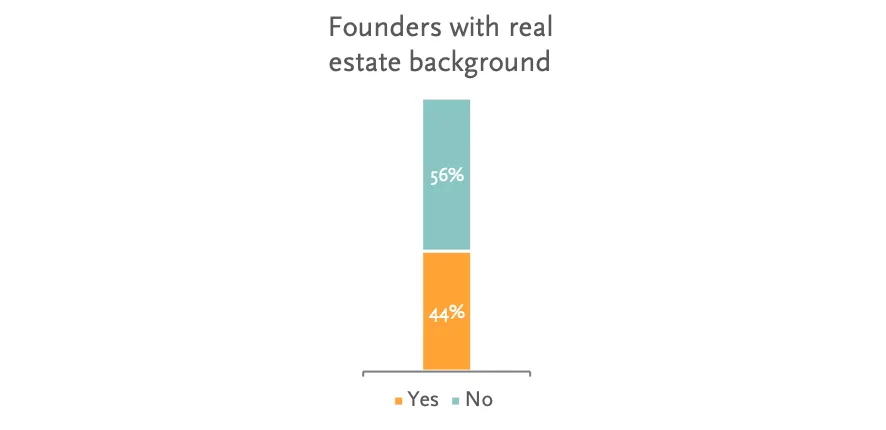

3. PropTech founders have real estate industry experience

In our communication with PropTech founders, we have repeatedly noticed that many of them have a strong understanding of the industry. Frequently (44%), they had previously worked in the industry for many years and experienced first hand where the need for optimization is most urgent.

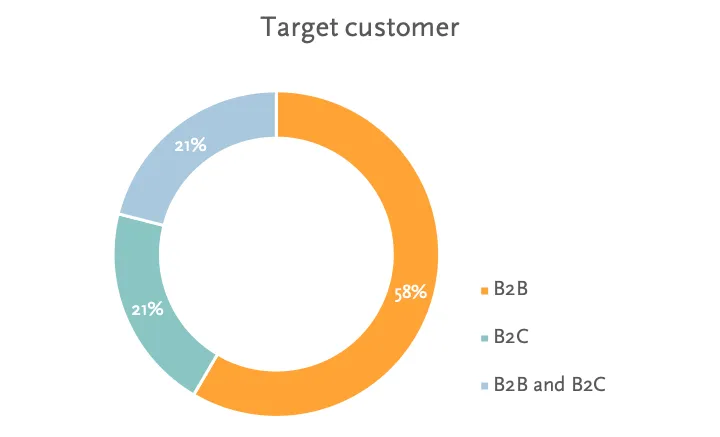

The founders urgently need a strong understanding of the industry, as almost 80% of the startups surveyed develop solutions for the real estate industry (B2B or B2B/B2C). This is a completely logical approach since the real estate sector with its established, but often completely unoptimized processes has an enormous economic volume and thus potential for PropTechs that enhance the efficiency. At the same time, the strong B2B overhang confirms our thesis that mastering traditional B2C acquisition channels such as performance marketing alone will bring only the fewest startups to success. Rather, the often stony path of B2B sales must be followed and a high-quality investor should also be able to generate corresponding added value here.

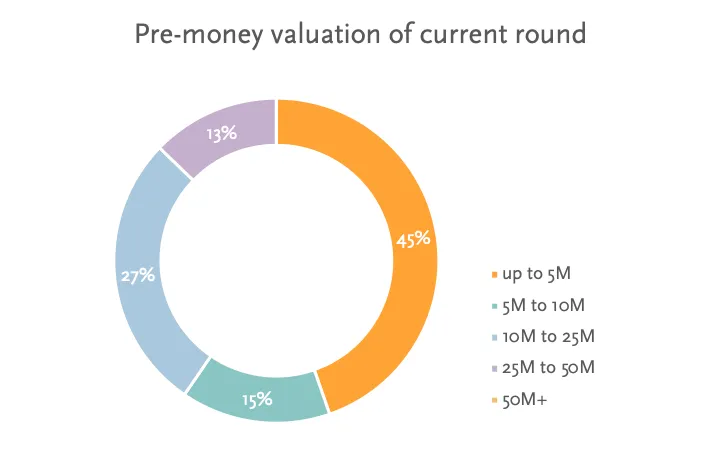

4. The PropTech sector still shows strong growth potential

The fact that the PropTech ecosystem is still under development is demonstrated by the relatively low company valuations. 45% of the companies we analyzed were looking for financing with a pre-money valuation of less than €5 million. 41% of companies have already passed the €10 million mark. Growth stage companies valued at more than €25 million are still rather rare at 14%. Company valuations of more than €50 million are the absolute exception. Overall, our sample thus shows an average valuation of a moderate €12 million.

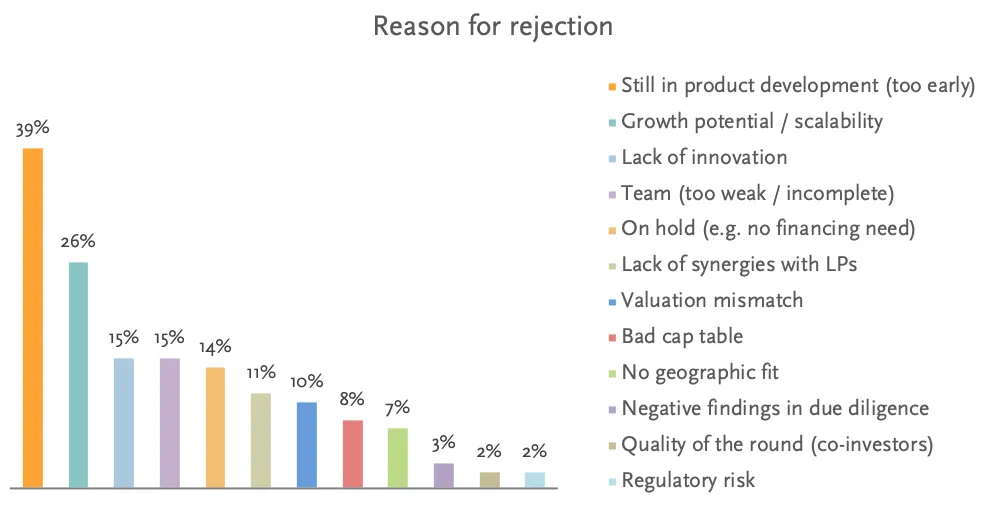

When assessing the reasons for rejection, it should be noted that several factors often come together or that one and the same rejection process allows for a categorization as both “too early” and “too expensive” since often several points of criticism represent only two sides of the same coin. All in all, the valuation on which the round is raised often plays an important role in the decision-making process. 39% of our pitches fall through the grid because the products are still in the (too early) process of being developed. On the one hand, this may be due to the fact that the startup is simply not yet in the right phase for a VC investment and, for example, is initially better served with a business angel investment. On the other hand, however, it may also be due to the fact that the valuation expectations for the (not yet delivered) KPIs are too high. PropTechs should also pay attention to sufficient scalability and the potential market size in early phases because this is the second most frequent reason for rejection, as venture capital in particular requires a scaling potential of roughly a factor 10 of the valuation at which the round is being raised. A team that is too inexperienced or does not complement each other as well as a lack of innovation are next on the list.

5. Traditional real estate companies do not want to be left behind by digitization

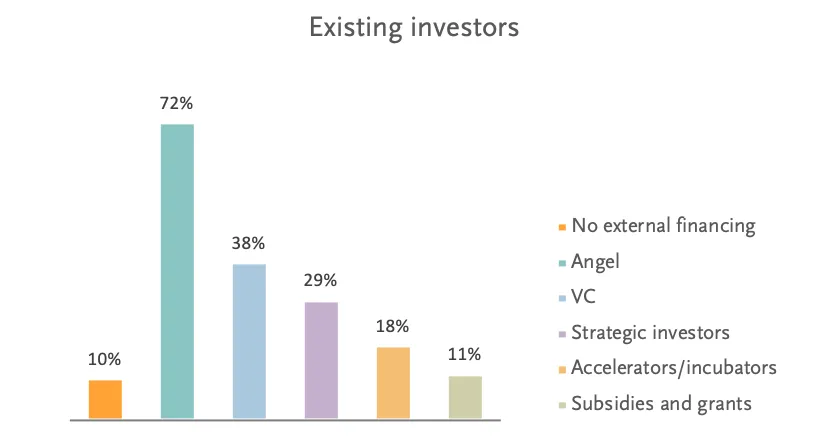

If we take a look at the cap tables of the startups, it is noticeable that most of them have already secured external capital before they end up on the tables of our investment managers. As usual, business angels are most frequently represented with 72%, but almost 30% of PropTechs have already secured strategic investors from the industry. This is not surprising, especially in the context of the outlined B2B predominance, because it is in the interest of corporates to not simply watch the digital development from the sidelines, but to be actively involved in the development of the companies. Overall, we were able to record an increasing diversification of the PropTech investor landscape.

Why strategic direct investments are not the magic bullet

It is not surprising that many market participants from the real estate industry become active in the PropTech environment since industries such as retail, finance, and media have provided more than enough illustrative material in the recent past that a passive attitude in times of increasing digitalization leads to one’s own downfall. However, a good year after the launch of PropTech1, we still believe in the advantages of neutral financial investors versus classic direct investments by strategic investors, especially in early phases of a company.

The best startups often react almost allergically to strategic investors. On the one hand, this is due to the fear that a startup, with the inclusion of a strategic investor in the cap table, will practically seal itself off from its competitors — whether as a customer, future investor, or even buyer. This competitive disadvantage is particularly noticeable with B2B business models in the real estate sector, as there are often only a few players of significant size in the specific segments along the value chain, and the barriers between those players have usually been raised accordingly.

On the other hand, startups fear the — who would have thought it — strategic interests of a strategic investor. While the primary goal of a startup is growth, the financial return generated from the investments of the corporates plays a subordinate role in their own balance sheet. Therefore, they often pursue strategic goals, such as purposefully isolating the startup from the rest of the market in order to deny their competitors the added value of the startup or to prevent a sale of the startup — and thus of their own data.

Although there are laudable exceptions and harmonious cooperations between startups, corporates, and financial investors (e.g. in our portfolio company Architrave), generally speaking the interests of pure financial investors and startups often converge or are at least substantially more transparent and thus more predictable.

As a result, strategic investors who focus exclusively on direct investments often risk an adverse selection, as the best startups select the — subjectively — best investors.

Even after just over a year of investment activity, we are therefore convinced of our approach to externally, i.e. vis-à-vis the startups, act purely as an independent financial investor with PropTech1. At the same time, however, we can offer startups the same or often even more added value than a single strategic investor due to a large number of real estate companies and entrepreneurs as shareholders in our fund (today already more than 20, with increasing tendency).

We also create an additional way for our shareholders to invest in startups alongside their own direct investment activities and therefore, from their point of view, permit multi-track program management with both direct and indirect investments — and thus a “best of both worlds”.